Mô tả

Global Steel Market

Production: Global crude steel production in March 2026 reached 159.9 million tons, down 4.2% compared to the same period in 2025. Overall, in Q1 2026, global production decreased by 2.3%, with China experiencing a 4.6% decline, while India and the US maintained strong growth (10.8% and 5.7% respectively).

Trade: Protectionist trends are increasing as the UK officially doubled import tariffs on steel exceeding quotas to 50% from July 1st.

Prices: Hot-rolled steel (HRC) prices rose sharply in the EU (up approximately 5.8-5.9%) and the US (up 3.3%) in March due to factory price adjustments and the impact of the CBAM mechanism.

Forecast: Global steel demand is expected to grow slightly by 0.3% in 2026 and recover more strongly to 2.2% in 2027.

China Steel Market

Production: Crude steel output in Q1 reached 247.55 million tons, down 4.6% year-on-year. Profit margins for mills narrowed significantly due to high input costs (iron ore, coking coal) while domestic demand from real estate remained very weak.

Trade: Steel exports in Q1 decreased by 9.9% and imports decreased by 14.1% due to increased trade barriers and low domestic demand.

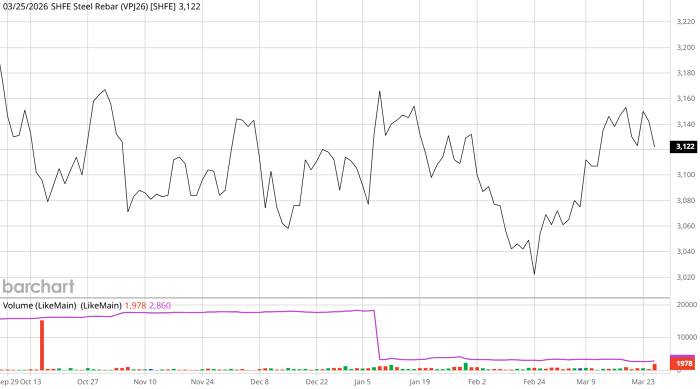

Prices: Shanghai rebar futures prices only increased slightly by 0.5% year-on-year, indicating the market is still in a correction phase and unable to break through due to high inventory pressure.

Vietnam Steel Market

Production: A strong recovery was recorded with crude steel production in Q1 reaching over 7.16 million tons (up 23.3%) and finished steel production reaching over 8.53 million tons (up 14.4%) — the highest level in the past 5 years.

Consumption: Finished steel sales in Q1 reached 8.66 million tons, up 15.5%. The biggest highlight was the surge in construction steel sales, up 29.1%, driven by public investment (disbursement reached 11% of the plan), the start-up of real estate projects, and social housing projects.

Exports: Total finished steel exports in Q1 reached 1.29 million tons, down 8.2% due to trade protection barriers in various countries. However, HRC was a "bright spot" with export volume more than doubling thanks to taking advantage of supply disruptions from Iran.

Price developments: Continuous increases in input material prices are putting pressure on "cost-push" prices. Domestic construction steel prices in Q1 saw 4-6 upward adjustments, with a total increase of VND 1,200 - VND 1,450/kg.

Forecast: Consumption demand is expected to remain positive until the end of Q2/2026. Construction steel prices could soon reach VND 16 million/ton if geopolitical conflicts continue to drive up energy and logistics costs.

Businesses: Steel manufacturers like Hoa Phat continued to record a positive business quarter. In contrast, the galvanized steel sheet sector continued to have a bleak business outlook amidst weakening exports due to increased protectionism and fierce competition from Chinese steel in the international market.

.png)

.png)